import matplotlib.pyplot as plt

import seaborn as sns

import numpy as np

from scipy.stats import gamma, norm

from scipy.optimize import minimize_scalar

sns.set(style="whitegrid")

colors = sns.color_palette("Paired")

4. Laplace’s Method Demo*#

Steps#

As we learned in the last lecture, these are the steps to Laplace approximation:

Find the mode.

The mean of the approximating normal distribution will be the mode, or maximum a posteriori probability (MAP) solution, of the posterior.

We solve for the MAP by maximizing the unnormalized posterior with respect to \(\theta\) or by maximizing the log of the unnormalized posterior:

Find the variance.

In the lecture notation:

Normal approximation:

The Laplace approximation to the posterior is a normal distribution with mean \(\hat{\theta}\) and variance \(Q^{-1}\):

Univariate example#

From Unit 5: laplace.m.

Here’s our example model:

Since this is a conjugate model, we already know the exact posterior is \(Ga(r+\alpha, \beta +x)\). We know the mode is \(\frac{r + \alpha - 1}{\beta + x}\), but let’s pretend we don’t.

Mode#

In this case it’s not too tough to find the mode analytically.

The log of the unnormalized posterior is \(\log g(\theta) = (r + \alpha - 1)\log(\theta) - (\beta + x)\theta\), so we can just take the derivative and set it equal to zero, then solve for \(\theta\):

For this example our given parameters are \(r=20, \alpha=5, \beta=1, x=2\), so our mode is equal to \(8\).

We could also use optimization:

# define our posterior

def neg_log_post(θ, r, α, β, x):

return -((r + α - 1) * np.log(θ) - (β + x) * θ)

r, α, β, x = 20, 5, 1, 2

result = minimize_scalar(

neg_log_post, bounds=(0, 1e6), args=(r, α, β, x), method="bounded"

)

mode = result.x

print(f"Mode: {mode}")

Mode: 8.000001689177818

Variance#

The true variance of the posterior is \(\frac{r+\alpha - 1}{(\beta + x)^2}\).

The approximation distribution’s variance will be:

Compare the true posterior with the approximation#

xx = np.linspace(0, 16, 100000)

variance = (mode**2) / (α + r - 1)

# normal parameters

mu = mode

sigma = variance**0.5

# gamma parameters

shape = r + α

scale = 1 / (β + x)

exact = gamma.pdf(xx, a=shape, scale=scale)

approx = norm.pdf(xx, mu, sigma)

# credible intervals

exact_ci = gamma.ppf(0.025, a=shape, scale=scale), gamma.ppf(

0.975, a=shape, scale=scale

)

approx_ci = norm.ppf(0.025, mu, sigma), norm.ppf(0.975, mu, sigma)

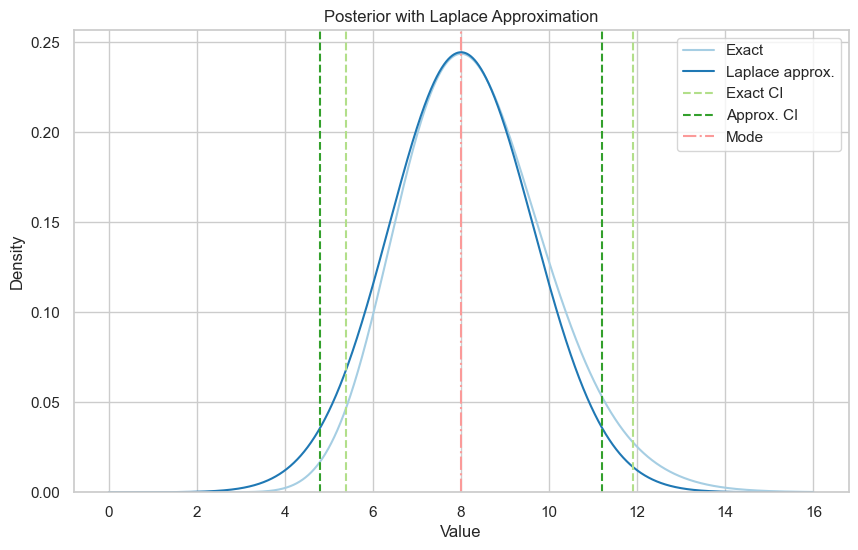

print(f"Exact 95% credible interval: {exact_ci}")

print(f"Laplace approximation 95% credible interval: {approx_ci}")

Exact 95% credible interval: (5.392893949276442, 11.903365864584403)

Laplace approximation 95% credible interval: (4.799393229141485, 11.20061014921415)

Show code cell source

# plotting code

plt.figure(figsize=(10, 6))

plt.plot(xx, exact, label="Exact", color=colors[0])

plt.plot(xx, approx, label="Laplace approx.", color=colors[1])

plt.axvline(x=exact_ci[0], color=colors[2], linestyle="--", label="Exact CI")

plt.axvline(x=exact_ci[1], color=colors[2], linestyle="--")

plt.axvline(x=approx_ci[0], color=colors[3], linestyle="--", label="Approx. CI")

plt.axvline(x=approx_ci[1], color=colors[3], linestyle="--")

plt.axvline(x=mode, color=colors[4], linestyle="-.", label="Mode")

plt.title("Posterior with Laplace Approximation")

plt.xlabel("Value")

plt.ylabel("Density")

plt.ylim(bottom=0)

plt.legend()

plt.show()

The exact posterior is a bit skewed to the right, so the normal approximation is a bit off, but it’s not too bad.

%load_ext watermark

%watermark -n -u -v -iv

Last updated: Sat Feb 24 2024

Python implementation: CPython

Python version : 3.11.5

IPython version : 8.15.0

numpy : 1.25.2

matplotlib: 3.7.2

seaborn : 0.13.0